The Economic and Political Weekly (EPW) is an important source of study material for IAS, especially for the current affairs segment. In this section, we give you the gist of the EPW magazine every week. The important topics covered in weekly are analysed and explained in a simple language, all from a UPSC perspective.

TABLE OF CONTENTS

1. Small Finance Banks: Creating Value for Stakeholders 2. Slow Vaccination Rate: A Sword of Damocles over the Economy

1. Small Finance Banks: Creating Value for Stakeholders

Context

The article highlights the instrumental role of Small Finance Banks (SFBs) in value creation for their stockholders and accelerating financial inclusivity.

Introduction

- SFBs promote institutional mechanisms to mobilize savings from rural and semi-urban areas and provide credit to viable economic entities in local areas.

- The SFBs are authorized to sell mutual funds, pensions, insurance, and other financial products and services to their customers.

- SFBs primarily focus on certain market segments such as small and marginal farmers, micro and small enterprises, and unorganized sector entities.

History

- The Government of India experimented with the SFB format in August 1996 to provide low-cost, efficient, and competitive financial services in semi-urban and rural India by issuing licenses to local area banks.

- Local area banks (LABs) cannot borrow funds from the RBI as they are non-scheduled banks.

- RBI issued licenses to 10 LABs and only four LABs are operating satisfactorily presently.

- In September 2015, RBI issued provisional licenses to 10 entities, mostly microfinance institutions, to convert themselves into SFBs within a period of one year.

- Presently, three SFBs – AU Small Finance Bank, Ujjivan Small Finance Bank, and Equitas Small Finance Bank have been listed both on the National Stock Exchange and the Bombay Stock Exchange.

Financial Inclusion

- In 2015, RBI issued licenses to establish the SFBs with a typical business model of 75:50:25.

- The business model of 75:50:25 suggests that SFBs need to direct 75% of the adjusted net bank credit towards priority sector lending, and 50% of the loans must be less than 25 lakh.

- SFBs can expand across India, subject to the condition that 25% of their branches should be in an unbanked area.

- SFB can also be converted into a full-fledged universal bank based on its satisfactory track record of performance and compliance with the RBI’s prudential norms.

- RBI recently allowed payment banks to get converted into SFBs after the completion of five years of their operations.

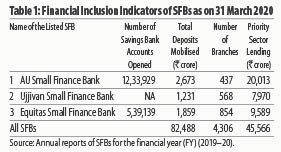

- According to RBI’s data, all the SFBs together have mobilized total deposits of Rs.82,488 crores and provided a credit of Rs.90,576 crores by the end of FY 2019–20.

- Total priority sector loans of the SFBs stood at Rs.45,566 crores, out of which micro, small and medium enterprises (MSMEs) had a major share of 35.8% followed by agriculture and allied sectors (23%) as of March 2020.

CAMELS Rating

- The United States Federal Reserve, in the 1980s, introduced CAMELS rating as a system of evaluating the banks for on-site examination and performance.

- The term CAMELS stands for Capital adequacy, Asset quality, Management, Earnings, Liquidity, and Sensitivity of banks.

- CAMELS rating assesses the performance of banks and it is the most popular approach to evaluate the performance of banks across the world and to suggest relevant measures to improve their shortcomings.

Assessment of SFBs

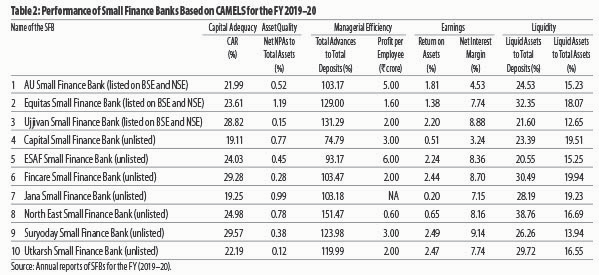

- RBI adopted the CAMELS rating approach in 1996 as per the recommendations of the Padmanabhan Committee (1995).

- SFBs are expected to have capital adequacy of 11.5% as per the norm of RBI.

- SFBs have abundant capital adequacy and met this criterion for the FY 2019–20 which can be understood from Table 2 below.

- It allows a lot of scope for increasing SFBs’ loan portfolios.

- Return on assets (RoA) and net interest margin (NIM) are the most commonly used indicators of the profitability of a bank.

- A higher ratio of RoA shows the efficient deployment of a bank’s assets.

- Seven out of 10 SFBs had RoA of over and above 1% which shows decent profitability of these banks as of 31 March 2020.

SFBs and Stock Exchange

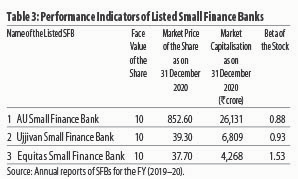

- According to RBI’s guidelines, the SFBs have to mandatorily get listed on a recognized stock exchange within three years after reaching a net worth of Rs.500 crore.

- SFBs’ listing will give scope for mobilization of additional capital through widely held ownership of shares, exit route to existing investors, ready marketability and price discovery of the shares, timely disclosure of financial results, better corporate governance, and monitoring.

- The performance of listed SFBs can be understood from the following table.

Conclusion

- The SFBs create value by providing last-mile connectivity in terms of digital and financial inclusion apart from imparting financial literacy.

- India should encourage the SFBs by creating the right environment in terms of ease of doing business, inducing competition among the SFBs through the listing, and changing goal posts in digital as well as financial inclusion.

- The SFBs may collaborate with centres of excellence and non-governmental organizations to impart financial literacy to their customers in order to scale up their operations and keep their asset quality intact.

- The banking system of a country significantly influences its economy and SFBs are the right vehicles to achieve digital and financial inclusion.

2. Slow Vaccination Rate: A Sword of Damocles over the Economy

Context

The article highlights the demand and supply-side events in the Indian Economy and the consecutive outcomes in the wake of the pandemic.

Highlights

- The first year of the pandemic had a devastating impact on the Indian economy as the GDP growth rate for the year 2020-21 highlights the crawling pace of the economic recovery.

- India has witnessed a marginal pickup in growth from 0.5% in the third quarter of 2020–21 to 1.6% in the fourth quarter of the financial year 2020-21.

- The annual GDP fell by 7.3% in 2020–21 accounting for the highest decline in the economy since independence.

- The per capita income fell by 8.4% in real terms and per capita private consumption fell by 10.1%.

Demand-side of the Economy

- The revival of both private and government consumption expenditures, which account for around 55% and 10% of the overall demand in the economy, has a key role in the pickup.

- There has been a 2.7% recovery in private consumption.

- Investments have prolonged across fixed capital and valuables though it remains considerably skewed.

- Government and private consumption expenditure registered contrasting trends in 2020–21.

- The investments in valuables rose by 1.9% while the capital investments fell.

- The 2.9% rise in government consumption expenditure could not compensate for the 8% decline in total private consumption.

- This skewed pickup in consumption and investment demand underlines the fragile and sluggish nature of incipient recovery.

Supply-side of the Economy

- The fourth-quarter recovery was primarily limited to sectors like construction, manufacturing and finance, real estate and professional services, and utility services like electricity, gas, and water supply.

- The growth of 3.1% in agriculture is a good sign for the rural economy in such a slowdown.

- The annual numbers show that agriculture and utilities had a positive growth of 3.6% and 1.9% in 2020–21.

- Other major sectors like trade, communication, hotels, transport, and other services had a decline in growth.

The Outbreak of the Second Wave

- The second wave is largely concentrated in states like Maharashtra, Karnataka, Kerala, Tamil Nadu, Delhi, Uttar Pradesh accounting for two-thirds of the infections.

- The significant decline in economic activities in these states (account for more than half the GDP) will dampen the growth prospects in the first quarter of 2021–22.

- Acceleration of vaccination rates to reduce the intensity of the disease seems like the only immediate solution.

- People might face the prospect of sinking back into the poverty trap in the present times with limited reliefs like food packages and MGNREGA.

Conclusion

- India is in urgent need of a large vaccination drive in order to rescue its people and economy; there are massive challenges of life and livelihood, job loss, and poverty trap.

- Economy, both demand and supply-side, shows a huge downfall which needs an externality of stimulus packages.

Read previous EPW articles in the link.

EPW June Week 1, 2021:- Download PDF Here

Comments