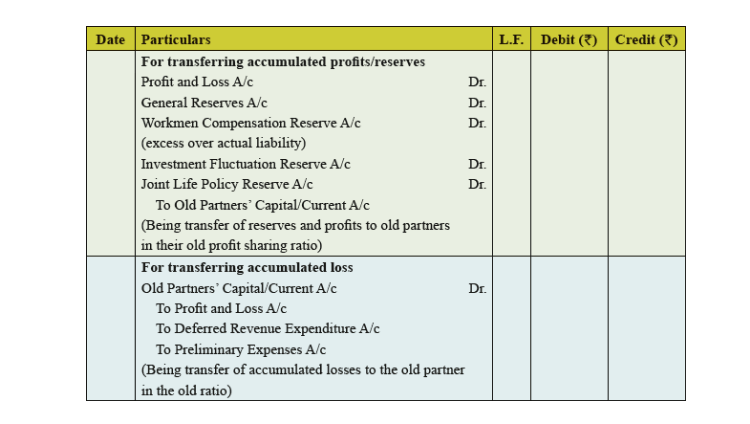

Accumulated Profits and Losses is the sum of an enterprise’s profits and losses left, after the dividend is paid. It can also be termed as either retained capital, retained earnings or earned surplus.

Sometimes, an enterprise might have accrued profits but not yet transferred to capital accounts of the partners. These are usually in the form of general reserve, reserve fund and/or Profit and Loss account balance. However, the new partner is not entitled to have any share in such accumulated profits. These are only allocated among the old partners by transferring it to their capital A/c in old profit sharing ratio. Correspondingly, if there are some accrued losses in the form of a Dr (Debit) balance of Profit and Loss account appearing in the balance sheet of the firm.

The journal entries for the Accumulated Profits and Losses account is as follows:

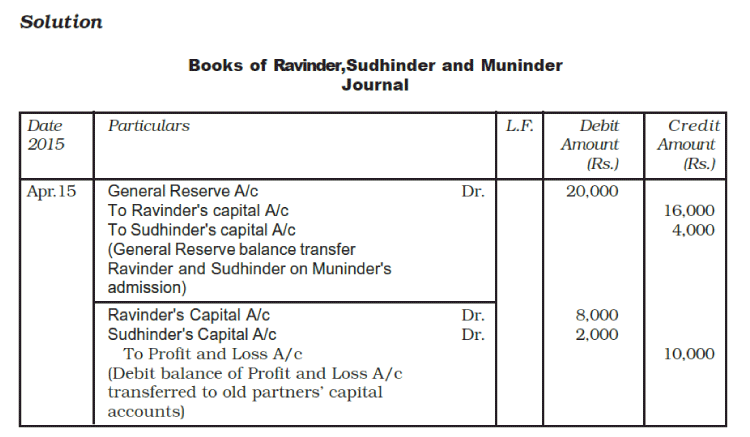

Below is an illustration mentioned for the clear picture :

Ravinder and Sudhinder are partners in an enterprise sharing profits in the ratio of 4:1. On 15th of April, 2015 they admit Muninder as a new partner. On that date there was a balance of Rs. 20,000 in general reserve and a debit balance of Rs. 10,000 in the profit and loss account of the firm. Pass necessary journal entries regarding the adjustment of a accumulate a profit or loss.

The above mentioned is the concept that is explained in detail about Adjustment for Accumulated Profits and Losses for the Class 12 Commerce students. To know more, stay tuned to BYJU’S.

Comments