Final Accounts Meaning

Final accounts are those accounts that are prepared by a joint stock company at the end of a fiscal year. The purpose of creating final accounts is to provide a clear picture of the financial position of the organisation to its management, owners, or any other users of such accounting information.

Final account preparation involves preparing a set of accounts and statements at the end of an accounting year. The final account consists of the following accounts:

- Trading and Profit and Loss Account

- Balance Sheet

- Profit and Loss Appropriation account

Objectives of Final Account preparation

Final accounts are prepared with the following objectives:

- To determine profit or loss incurred by a company in a given financial period

- To determine the financial position of the company

- To act as a source of information to convey the users of accounting information (owners, creditors, investors and other stakeholders) about the solvency of the company.

The format of a final account is represented as follows:

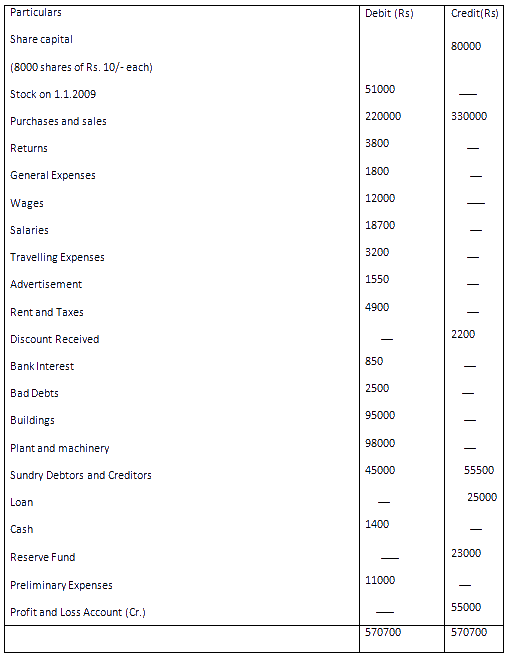

Q. Following is the Trial Balance of Rajesh Ltd., Gurgaon as on 31.12.2009.

Adjustments:

1. Transfer Rs. 10000 to Reserve Fund.

2. Provide depreciation on building at 5%.

3. Stock on 31.12.2009 was valued at Rs. 12000.

4. Dividend at 15% on share capital is to the provided.

5. Depreciation on Plant and Machinery at 10%.

Prepare Trading, Profit and Loss Account, Profit and Loss Appropriation Account and Balance Sheet in the prescribed form.

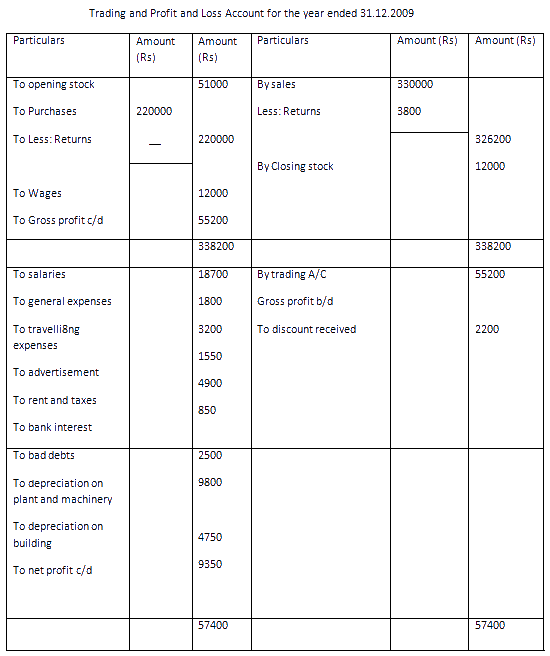

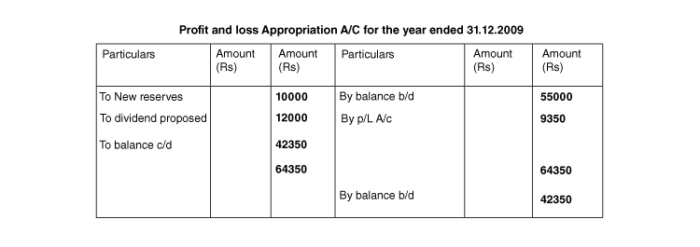

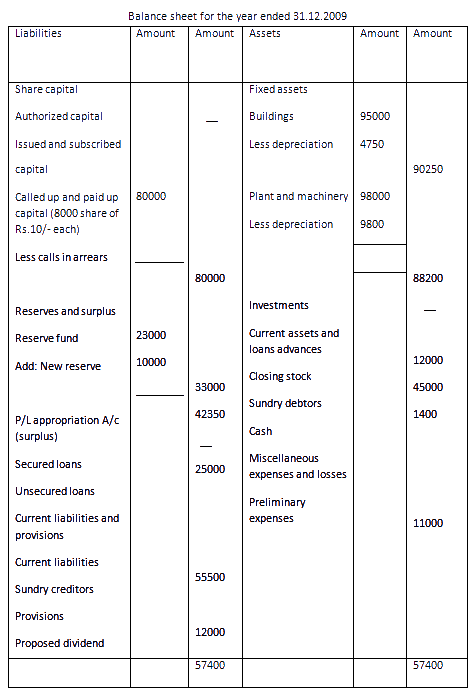

Solution:

The solution will be as follows:

The above mentioned is the concept that is explained in detail about Final Accounts for the Class 12 students. To know more, stay tuned to BYJU’S.

| Important Topics in Accountancy: |

Frequently Asked Questions on Final Account

What are the components of final accounts?

The components of final accounts are :

- Trading account

- Profit and loss account

- Profit and loss appropriation account

For manufacturing companies, a manufacturing account is prepared in addition to all the other accounts.

How many types of final accounts are there?

There are generally three types of final accounts and they are:

- Trading account

- Profit and loss account

- Balance sheet

What are the different stages of the final account of the company?

Different stages of final account of a company are:

- Prepare trial balance

- Adjusting the trial balance

- Preparing adjusted trial balance

- Prepare financial statements

- Closing the books

How do you calculate final accounts?

Final accounts can be calculated as follows:

- Make a list of trial balance items and adjustments

- Record debit items on expense side of P and L account or assets side in balance sheet

- Record credit items on the income side of trading P and L account or liabilities side of balance sheet.

- Balance the profit and loss account and determine profit or loss from the trial balance

- Add any profit obtained to the capital on the liabilities side of the balance sheet.

- Make a total of the balance sheet.

Give an example of the final account?

Profit and loss account is an example of a final account.

ok its very nice.

Nice

It’s a very useful to me. Thanks

excellent

Really helpful 👍

Thanks mam its very usefull to learn 👍

It’s very helpful to me. Thanks

Nice

Very helpful for me thank you so much.

Very helpful for me thank you

nice

nice